Regulated utilities make a big trade-off. They get a monopoly, but have to get their rates approved by the government. That often leads to slow but steady earnings and dividend growth over time. However, some utilities have been able to separate themselves from the slow-growth crowd. For example, American Water Works Company Inc. (NYSE:AWK), NextEra Energy Inc. (NYSE:NEE), and Dominion Energy Inc. (NYSE:D) are all targeting 10% dividend growth over the next few years. Here's a quick primer on each, if dividend growth that's three times the historical rate of inflation sounds good to you.

1. A water giant

American Water Works serves 1,600 communities in the United States and parts of Canada. It provides drinking water and wastewater services. The company's customers literally can't live without the water it provides. Growth comes from two main sources: upgrading its assets and acquiring new water systems in the highly fragmented water services industry.� �

Image source: Getty Images.

Spending to upgrade old water pipes is generally looked at favorably by regulators and helps get rate hikes approved. American Water Works plans to spend around $8 billion, largely on capital projects, over the next five years. That should help drive earnings higher by as much as 7%. Acquisitions, meanwhile, could add as much as two percentage points to the company's earnings growth (its nonregulated business could add another percentage point or two beyond that) and push spending up as high as $9 billion. And there are plenty of opportunities to buy assets -- American Water Works is the largest publicly traded water company, yet operates in only 16 states.�

All of that spending is expected to help American Water Works expand earnings and dividend between 7% and 10% a year through 2022. The most recent hike, which took place in the first quarter, was 9.6%. Although the yield is modest at 2.1%, the water utility's dividend growth is pretty impressive.� � �

2. The Sunshine State's dividend machine

NextEra Energy's regulated electric business provides power to 5 million customers in Florida. The state has seen its population grow over the years as people move from colder northern climates down to the warmth of the Sunshine State. That's a trend that doesn't appear to be changing, with Florida ranking second for population growth in 2017, trailing only Texas. More people means more customers for NextEra Energy's utility operations.� �

In addition to the push from population growth, NextEra has plans to spend as much as $19 billion on this segment of its business between 2017 and 2020. That spending includes things like general maintenance, upgrading power plants, and building new renewable-power projects. This spending should lead to positive relationships with regulators and improving rates.� �

NextEra also owns the largest renewable-power business in the world, according to the company. This nonregulated business is backed by long-term contracts and is fairly low risk. The utility plans to double its generating capacity in this division to 40 gigawatts by 2020. That's going to be a major growth driver for the company, backed by as much as $25 billion in spending between 2017 and 2020.� �

NextEra Energy's renewable power footprint. Image source: NextEra Energy

All in, the company is projecting earnings growth of 6% to 8% a year through 2021. Dividend growth, meanwhile, is expected to be between 12% and 14% through 2020. The most recent increase was made in the first quarter and was roughly 13%. That's huge dividend growth, but a relatively low payout ratio provides ample room to support such increases, and a higher payout ratio, over the next few years. Although NextEra Energy's dividend yield is modest for a utility, at 2.7%, its dividend growth history and potential are highly attractive.�� �

3. High yield and high dividend growth

Dominion Energy is by far the most diversified utility here, with operations broken down among electric transmission, power generation (both regulated and nonregulated), and natural gas delivery and transmission. Included in this mix is a controlled limited partnership, Dominion Energy Midstream Partners LP, through which the parent controls natural gas midstream assets.

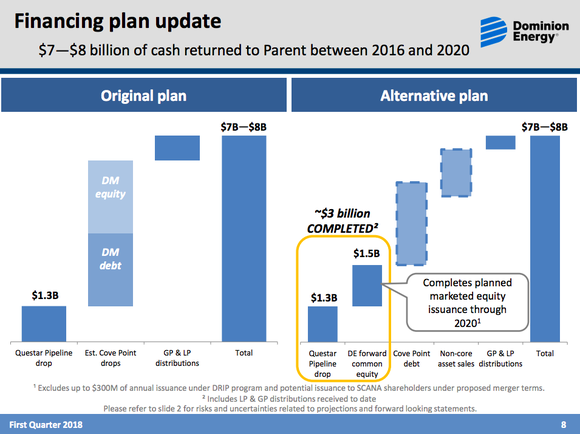

Dominion is planning to spend as much as $4.2 billion a year across its various businesses over the next few years. On the regulated electric side of the business, spending on things like new generating capacity should help support rates. On the non-regulated side, spending should expand the company's collection of assets, spurring growth. Overall, Dominion is projecting 6% to 8% annualized earnings growth through 2020, with dividend hikes of as much as 10% a year.� �

Dominion is by far the highest-yielding company of these three, with a dividend yield of 5.1%. There's a combination of factors behind this. For example, Dominion Energy Midstream Partners was expected to be a key capital source as Dominion Energy sold the controlled partnership assets (dropping them down, in industry lingo). However, a downturn in the midstream sector has caused Dominion Energy to step back from this plan. That means Dominion will have to add debt or sell equity to fund its growth, something investors were already worried about.

Dominion Energy's funding plan is in flux becuase of the low unit price for Dominion Energy Midstream Partners, L.P.

The utility is also trying to acquire financially troubled, smaller rival SCANA Corporation. Dominion doesn't expect the deal to change its dividend growth projections, but it will leave the utility responsible for cleaning up SCANA's scuttled nuclear power plant construction project. That's another issue that investors aren't happy about.� �

All in, Dominion probably has the riskiest outlook of this trio. But, for more aggressive investors, collecting the 5.1% yield while waiting for the utility to work through its current issues may be well worth it. Particularly since it is still calling for dividend growth of as much as 10% a year through 2020.

Not your grandmother's utilities

If you thought utilities were boring investments that only the most risk averse investors would be attracted to, then the dividend growth potential at American Water Works, NextEra Energy, and Dominion might surprise you. Although each company has a unique story, Dominion's particularly so, they are all worth a deep dive if you are looking for dividend growth. After a closer look, you might find that one or more has a place in your dividend growth portfolio.