Friday, March 22, 2019

Contrarians Combine As Canadian Titan Brookfield Buys Credit Heavyweight Oaktree Capital

Tuesday, March 19, 2019

Top 10 Heal Care Stocks To Own For 2019

If your portfolio doesn't have any exposure to renewable energy, then you may want to start thinking of that as a shortcoming. Why?

The United States sourced at least 15% of its electricity from hydroelectric dams, wind farms, and solar arrays in 2018. The growing trend will become undeniable in the next decade. This year wind power will topple hydropower as the nation's leading renewable energy source -- a title that had been held for over 100 years. Meanwhile, battery prices are falling at such a precipitous rate many projections call for solar energy to eventually eclipse both of its renewable peers. In fact, the U.S. Department of Energy thinks that could happen sometime around 2030 when the country is expected to lean on wind and solar alone for as much as 30% of its electricity.

Then again, most long-term projections have proven to underestimate the growth of wind and solar. The point is that growth-minded investors may want to begin searching for profitable businesses in renewable energy to own for the long haul. NextEra Energy Partners (NYSE:NEP) and Brookfield Renewable Partners (NYSE:BEP) are good places to start, especially considering both stocks are being disrespected by Wall Street at the moment.

Top 10 Heal Care Stocks To Own For 2019: Civeo Corporation(CVEO)

Advisors' Opinion:- [By Steve Symington]

Still, several individual companies easily outran the broader market. Read on to learn why shares of ManTech International (NASDAQ:MANT), Civeo (NYSE:CVEO), and Deutsche Bank (NYSE:DB) each climbed higher today.

- [By Lisa Levin]

Check out these big penny stock gainers and losers

Losers World Fuel Services Corporation (NYSE: INT) tumbled 18 percent to $22.90 following Q1 results. Biglari Holdings Inc. (NYSE: BH) fell 17.4 percent to $349.52. Washington Prime Group will replace Biglari Holdings in the S&P SmallCap 600 on Tuesday, May 1. Flex Ltd. (NASDAQ: FLEX) dipped 15.7 percent to $14.03 after a mixed fourth quarter report. FormFactor, Inc. (NASDAQ: FORM) fell 15.3 percent to $11.65. FormFactor is expected to release Q1 results on May 2. Data I/O Corporation (NASDAQ: DAIO) dropped 14.3 percent to $6.24 following Q1 results. National Instruments Corporation (NASDAQ: NATI) fell 14.3 percent to $ 42.34 after reporting Q1 results. United States Steel Corporation (NYSE: X) dipped 14.2 percent to $32.37 following Q1 results. Civeo Corporation (NYSE: CVEO) dropped 13.5 percent to $3.33. Civeo posted a Q1 loss of $0.42 per share on sales of $101.504 million. athenahealth, Inc. (NASDAQ: ATHN) fell 12.4 percent to $125.310 after reporting Q1 results. Charter Communications, Inc. (NASDAQ: CHTR) shares tumbled 12.1 percent to $262.06 as the company posted Q1 results. Value Line, Inc. (NASDAQ: VALU) fell 11.3 percent to $19.10. Federated Investors, Inc. (NYSE: FII) shares dropped 11.2 percent to $27.605 after the company posted downbeat quarterly earnings. AV Homes, Inc. (NASDAQ: AVHI) declined 10.7 percent to $17.20 following Q1 results. CalAmp Corp. (NASDAQ: CAMP) dropped 9.4 percent to $21.01 after reporting Q4 results. Tandem Diabetes Care, Inc. (NASDAQ: TNDM) shares fell 8.9 percent to $7.280 following mixed Q1 results. Sony Corporation (NYSE: SNE) shares fell 8.4 percent to $45.97 after reporting Q4 results. LogMeIn Inc (NASDAQ: LOGM) fell 8.2 percent to $109.825. LogMeIn reported upbeat earnings for its first quarter, but issued weak second quarter and FY18 earning guidance. Eleven Biotherapeutics, Inc. (NASDAQ: EBIO - [By Logan Wallace]

Civeo Corp (NYSE:CVEO)’s share price was up 5.8% during trading on Tuesday . The stock traded as high as $3.53 and last traded at $3.48. Approximately 766,001 shares changed hands during mid-day trading, an increase of 1% from the average daily volume of 754,849 shares. The stock had previously closed at $3.29.

- [By Shane Hupp]

Civeo (NYSE:CVEO) was downgraded by research analysts at ValuEngine from a “buy” rating to a “hold” rating in a note issued to investors on Monday.

Top 10 Heal Care Stocks To Own For 2019: Nam Tai Property Inc.(NTP)

Advisors' Opinion:- [By Ethan Ryder]

News coverage about Nam Tai Property (NYSE:NTP) has trended somewhat positive recently, according to Accern. Accern rates the sentiment of media coverage by reviewing more than 20 million news and blog sources in real-time. Accern ranks coverage of companies on a scale of -1 to 1, with scores closest to one being the most favorable. Nam Tai Property earned a news impact score of 0.20 on Accern’s scale. Accern also gave news coverage about the electronics maker an impact score of 47.3059674665332 out of 100, indicating that recent media coverage is somewhat unlikely to have an effect on the company’s share price in the next few days.

Top 10 Heal Care Stocks To Own For 2019: Catalent, Inc.(CTLT)

Advisors' Opinion:- [By Max Byerly]

Catalent (NYSE:CTLT) SVP Steven L. Fasman sold 2,252 shares of the firm’s stock in a transaction on Wednesday, June 20th. The shares were sold at an average price of $41.78, for a total transaction of $94,088.56. The transaction was disclosed in a filing with the Securities & Exchange Commission, which is available through this hyperlink.

- [By Joseph Griffin]

Get a free copy of the Zacks research report on Catalent (CTLT)

For more information about research offerings from Zacks Investment Research, visit Zacks.com

- [By Max Byerly]

Get a free copy of the Zacks research report on Catalent (CTLT)

For more information about research offerings from Zacks Investment Research, visit Zacks.com

- [By Logan Wallace]

Catalent Inc (NYSE:CTLT) – Investment analysts at Piper Jaffray Companies reduced their Q2 2019 earnings per share (EPS) estimates for Catalent in a research note issued on Tuesday, August 28th. Piper Jaffray Companies analyst S. Wieland now anticipates that the company will post earnings of $0.36 per share for the quarter, down from their prior forecast of $0.42. Piper Jaffray Companies also issued estimates for Catalent’s Q3 2019 earnings at $0.40 EPS, Q4 2019 earnings at $0.68 EPS and FY2019 earnings at $1.71 EPS.

- [By Motley Fool Transcribers]

Catalent Inc (NYSE:CTLT)Q2 2019 Earnings Conference CallFeb. 05, 2019, 8:15 a.m. ET

Contents: Prepared Remarks Questions and Answers Call Participants Prepared Remarks:Operator

Top 10 Heal Care Stocks To Own For 2019: Eaton Vance Limited Duration Income Fund(EVV)

Advisors' Opinion:- [By Logan Wallace]

Eaton Vance Ltd Duration Income Fund (NYSEAMERICAN:EVV) was the recipient of a large increase in short interest in September. As of September 14th, there was short interest totalling 61,700 shares, an increase of 154.4% from the August 31st total of 24,249 shares. Currently, 0.1% of the company’s shares are short sold. Based on an average trading volume of 199,358 shares, the short-interest ratio is currently 0.3 days.

Top 10 Heal Care Stocks To Own For 2019: Scudder Municiple Income Trust(KTF)

Advisors' Opinion:- [By Stephan Byrd]

Fiera Capital Corp raised its holdings in shares of Deutsche Municipal Income Trust (NYSE:KTF) by 46.0% in the second quarter, according to the company in its most recent filing with the Securities & Exchange Commission. The institutional investor owned 353,686 shares of the investment management company’s stock after purchasing an additional 111,410 shares during the quarter. Fiera Capital Corp’s holdings in Deutsche Municipal Income Trust were worth $3,898,000 at the end of the most recent quarter.

- [By Shane Hupp]

TRADEMARK VIOLATION NOTICE: “DWS Municipal Income Trust (KTF) Plans $0.04 Monthly Dividend” was posted by Ticker Report and is owned by of Ticker Report. If you are viewing this story on another site, it was copied illegally and republished in violation of US and international trademark & copyright law. The correct version of this story can be read at https://www.tickerreport.com/banking-finance/4150549/dws-municipal-income-trust-ktf-plans-0-04-monthly-dividend.html.

Top 10 Heal Care Stocks To Own For 2019: Kamada Ltd.(KMDA)

Advisors' Opinion:- [By Garrett Baldwin] Retail stocks are in focus after the U.S. Census Bureau released monthly sales figures before the bell Tuesday. The bureau said that retail sales increased by 0.3% in April, a figure that matched trade expectations. Markets had expected consumer spending to increase, however home improvement sales were not the major factor that most expected. This was evident from The Home Depot's earnings report. Markets are increasingly optimistic over U.S. trade negotiations with China. Chinese President Xi Jinping's No. 1 economic advisor will visit the United States this week to continue the nation's dialogue with America. In addition, roughly 100 companies and trade associations will be sounding off to the Trump administration about the potential impact of tariffs in the Chinese markets. Stocks to Watch Today: TSLA, AMZN, GS Amazon.com Inc. (Nasdaq: AMZN) is in focus thanks to tax policy in Seattle. On Monday, the Seattle's City Council passed a bill that will tax Amazon and 131 other companies $275 per employee each year in order to create a fund to address homelessness in the Seattle. The tax is half what was originally proposed and remains a contentious issue for Amazon, which is the city's biggest employer. Goldman Sachs Group (NYSE: GS) is sounding the alarm about the state of the markets. The company warned that the U.S. budget deficit is increasing while America's unemployment rate is falling. This hasn't occurred since the World War II. The bank believes that the combination of the two could cause the Fed to spike interest rates in the near future. This comes at a time when the Fed has already lost control of interest rates. Look for additional earnings reports from Eagle Materials Inc. (NYSE: EXP), Bitauto Holding Ltd. (Nasdaq: BITA), Virtusa Corp. (Nasdaq: VRTU), Global Eagle Entertainment Inc. (Nasdaq: ENT), and Kamada Ltd. (Nasdaq: KMDA).

Follow Money Morning on Facebook, Twitter, and LinkedIn.

- [By Joseph Griffin]

Get a free copy of the Zacks research report on Kamada (KMDA)

For more information about research offerings from Zacks Investment Research, visit Zacks.com

- [By Stephan Byrd]

Shares of Kamada Ltd. (NASDAQ:KMDA) have been given an average rating of “Buy” by the six analysts that are presently covering the firm, Marketbeat Ratings reports. Two analysts have rated the stock with a hold recommendation and three have issued a buy recommendation on the company. The average 1 year target price among brokerages that have updated their coverage on the stock in the last year is $8.33.

- [By Lisa Levin]

Kamada Ltd. (NASDAQ: KMDA) is expected to report quarterly earnings at $0.02 per share on revenue of $24.02 million.

Concordia International Corp. (NASDAQ: CXRX) is estimated to report quarterly earnings at $0.06 per share on revenue of $143.80 million.

- [By Ethan Ryder]

Kamada Ltd. (NASDAQ:KMDA) – Stock analysts at Jefferies Group dropped their FY2020 earnings estimates for shares of Kamada in a research report issued on Tuesday, May 15th. Jefferies Group analyst R. Denhoy now anticipates that the biotechnology company will earn $0.61 per share for the year, down from their previous forecast of $0.62. Jefferies Group also issued estimates for Kamada’s FY2021 earnings at $0.36 EPS.

Top 10 Heal Care Stocks To Own For 2019: QuinStreet, Inc.(QNST)

Advisors' Opinion:- [By Ethan Ryder]

QuinStreet Inc (NASDAQ:QNST) has been given a consensus rating of “Buy” by the nine brokerages that are currently covering the company, MarketBeat.com reports. One research analyst has rated the stock with a hold recommendation and six have issued a buy recommendation on the company. The average 1-year price target among brokerages that have issued ratings on the stock in the last year is $17.29.

- [By Joseph Griffin]

Get a free copy of the Zacks research report on QuinStreet (QNST)

For more information about research offerings from Zacks Investment Research, visit Zacks.com

- [By Joseph Griffin]

Parisi Gray Wealth Management bought a new stake in shares of QuinStreet Inc (NASDAQ:QNST) in the 4th quarter, HoldingsChannel reports. The institutional investor bought 2,932 shares of the technology company’s stock, valued at approximately $47,000.

- [By Ethan Ryder]

QuinStreet Inc (NASDAQ:QNST) saw strong trading volume on Friday . 1,534,725 shares were traded during mid-day trading, an increase of 131% from the previous session’s volume of 665,429 shares.The stock last traded at $13.79 and had previously closed at $13.59.

Top 10 Heal Care Stocks To Own For 2019: Extreme Networks Inc.(EXTR)

Advisors' Opinion:- [By Anders Bylund]

Shares of network equipment maker Extreme Networks (NASDAQ:EXTR) are having a rough Wednesday. The stock opened 26.8% lower today, following last night's release of disappointing third-quarter results.

- [By Joseph Griffin]

Extreme Networks (NASDAQ:EXTR) posted its earnings results on Wednesday. The technology company reported $0.20 earnings per share (EPS) for the quarter, beating the consensus estimate of $0.19 by $0.01, Bloomberg Earnings reports. Extreme Networks had a positive return on equity of 43.61% and a negative net margin of 3.28%. The company had revenue of $278.30 million for the quarter, compared to analyst estimates of $279.22 million. During the same quarter in the previous year, the firm earned $0.17 earnings per share. The firm’s quarterly revenue was up 55.6% compared to the same quarter last year. Extreme Networks updated its Q1 guidance to $0.00-0.07 EPS.

- [By Ethan Ryder]

Usca Ria LLC acquired a new position in shares of Extreme Networks, Inc (NASDAQ:EXTR) in the 2nd quarter, according to the company in its most recent 13F filing with the SEC. The fund acquired 12,821 shares of the technology company’s stock, valued at approximately $102,000.

- [By Lisa Levin]

Some of the stocks that may grab investor focus today are:

Wall Street expects Booking Holdings Inc. (NASDAQ: BKNG) to post quarterly earnings at $10.67 per share on revenue of $2.87 billion after the closing bell. Booking Holdings shares gained 0.99 percent to $2,183.00 in after-hours trading. Tripadvisor Inc (NASDAQ: TRIP) reported stronger-than-expected results for its first quarter on Tuesday. Tripadvisor shares climbed 20.55 percent to $46.75 in the after-hours trading session. Analysts are expecting Anheuser-Busch InBev SA/NV (NYSE: BUD) to have earned $0.89 per share on revenue of $13.06 billion in the latest quarter. Anheuser-Busch will release earnings before the markets open. Anheuser-Busch shares gained 0.77 percent to $99.00 in after-hours trading. Extreme Networks, Inc (NASDAQ: EXTR) reported downbeat earnings for its third quarter and issued weak Q4 guidance. Extreme Networks shares fell 28.51 percent to $8.40 in the after-hours trading session. Before the opening bell, Ameren Corporation (NYSE: AEE) is projected to report quarterly earnings at $0.57 per share on revenue of $1.55 billion. Ameren shares dropped 2.78 percent to close at $56.91 on Tuesday.Find out what's going on in today's market and bring any questions you have to Benzinga's PreMarket Prep.

Top 10 Heal Care Stocks To Own For 2019: Vanda Pharmaceuticals Inc.(VNDA)

Advisors' Opinion:- [By Shane Hupp]

Get a free copy of the Zacks research report on Vanda Pharmaceuticals (VNDA)

For more information about research offerings from Zacks Investment Research, visit Zacks.com

- [By Max Byerly]

Vanda Pharmaceuticals Inc. (NASDAQ:VNDA)’s share price traded up 9.2% during mid-day trading on Thursday following a better than expected earnings announcement. The company traded as high as $20.47 and last traded at $20.12. 2,452,372 shares changed hands during mid-day trading, an increase of 134% from the average session volume of 1,049,783 shares. The stock had previously closed at $18.42.

- [By Max Byerly]

Get a free copy of the Zacks research report on Vanda Pharmaceuticals (VNDA)

For more information about research offerings from Zacks Investment Research, visit Zacks.com

- [By Maxx Chatsko, Chris Neiger, and Neha Chamaria]

That's a great example to make investors rethink where they're looking for growth stocks. We recently asked three Motley Fool contributors for their top growth investments right now. Here's why they chose Vanda Pharmaceuticals (NASDAQ:VNDA), XPO Logistics (NYSE:XPO), and HubSpot (NYSE:HUBS).

Top 10 Heal Care Stocks To Own For 2019: Six Flags Entertainment Corporation New(SIX)

Advisors' Opinion:- [By Joseph Griffin]

Get a free copy of the Zacks research report on Six Flags Entertainment (SIX)

For more information about research offerings from Zacks Investment Research, visit Zacks.com

- [By Rick Munarriz]

Haunted mazes, scare zones, and a safe but sinister vibe have helped players prop up their financials during the fourth quarter, which has been a sleepy period in the past. It's not a surprise that Six Flags (NYSE:SIX) has posted more revenue growth in the fourth quarter than it has for the entire year in recent years.

- [By Lisa Levin] Gainers Daré Bioscience, Inc. (NASDAQ: DARE) shares climbed 54.2 percent to $1.25 on news that the company entered into worldwide license agreement for Juniper Pharmaceuticals' intravaginal ring technology platform. Travelzoo (NASDAQ: TZOO) climbed 21.3 percent to $9.40 following strong Q1 results. Intrepid Potash, Inc. (NYSE: IPI) gained 16.5 percent to $4.60. K12 Inc. (NYSE: LRN) shares rose 11.2 percent to $15.4206 following Q3 results. Chicago Bridge & Iron Company N.V. (NYSE: CBI) shares rose 11 percent to $15.3289. McDermott issued a release reiterating rejection of Subsea 7's offer. Six Flags Entertainment Corporation (NYSE: SIX) shares gained 9.2 percent to $64.61 as the company posted a narrower-than-expected loss for its first quarter. Tupperware Brands Corporation (NYSE: TUP) surged 8.5 percent to $46.00 as the company posted in-line quarterly earnings. Carlisle Companies Incorporated (NYSE: CSL) climbed 7.5 percent to $107.22 after reporting Q1 results. Allena Pharmaceuticals, Inc. (NASDAQ: ALNA) rose 6.1 percent to $14.78. B. Riley initiated coverage on Allena Pharmaceuticals with a Buy rating. Texas Instruments Incorporated (NASDAQ: TXN) rose 4.6 percent to $102.90 after the company reported stronger-than-expected earnings for its first quarter on Tuesday. Credit Suisse Group AG (NYSE: CS) rose 4.5 percent to $17.03 following strong Q1 results. STMicroelectronics N.V. (NYSE: STM) rose 4.2 percent to $22.20 after reporting Q1 results.

Check out these big penny stock gainers and losers

- [By Steve Symington]

Shares of Six Flags Entertainment Corp. (NYSE:SIX) were up 8.8% as of 2 p.m. EDT Wednesday after the theme park operator announced better-than-expected first-quarter 2018 results.

- [By Dan Caplinger]

Stocks rebounded on Wednesday, with the Dow Jones Industrial Average climbing back from triple-digit losses early in the session to finish with a modest gain. Market participants were initially nervous because of the continued upward pressure on interest rates and their potential negative impact on the U.S. economy. But later in the day, confidence returned, and the steadfast market reversed course. Several individual stocks had much larger advances. Norfolk Southern (NYSE:NSC), Six Flags Entertainment (NYSE:SIX), and Intrepid Potash (NYSE:IPI) were among the best performers on the day. Here's why they did so well.

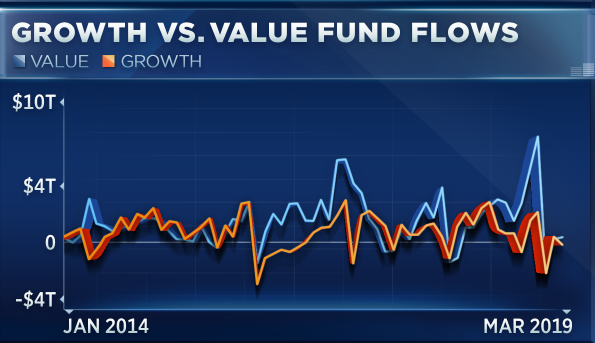

Sunday, March 17, 2019

Growth stocks set to rally this year, market watcher says

The S&P 500 has raced higher this quarter and one group of stocks has done the heavy lifting.

Growth stocks, prized for high sales and profit potential, have led the market higher since the December bottom.

Lindsey Bell, investment strategist at CFRA Research, said this is just the beginning of a bigger trend.

"Growth is going to continue to lead as [economic] growth picks up as the year carries on and I think that's because you've seen these stocks hit down a lot worse than some of the other areas of the market so they have a lot further to go from there," Bell said Thursday on CNBC's "Trading Nation."

Stocks with high-growth potential, such as the tech names, typically get a bid when the economy is strong as investors are more willing to pay a higher price for a bigger payoff. During a downturn, investors tend to hide out in value stocks which have lower valuations and more consistent profits.

As fears of an economic slowdown rose over the fourth quarter, both value and growth stocks were punished; the IVE value ETF plummeted 13 percent, while the IVW growth ETF saw a sharper 15 percent decline.

A low bar for earnings after the December sell-off could also be a catalyst for growth stocks, according to Bell.

"Earnings numbers have been cut drastically for these guys, way more than the S&P 500, way more than the value stocks so I think there just lies opportunity there when we do get that economic growth back," said Bell.

The Street anticipates earnings for growth stocks to fall by 0.6 percent this year, said Bell, far worse than initial expectations for an increase of 7.6 percent. By comparison, value earnings growth was reduced to 4.4 percent growth from 7.5 percent.

While money has flowed back into growth stocks after December's sell-off, Bell fears some investors may have been left out. ETF funds, a passive investment vehicle often used by individual investors, have shown flows into value indexes over growth since mid-2018.

"They're getting a little more nervous," Bell said of investor sentiment. "It's the later stages of this business cycle, we're in the 10th year of the bull market and they're just being a little more cautious with the uncertainties that still remain out there."

However, even if a recession was on the horizon, historical returns suggest growth stocks still deliver.

"Investors should consider the growth area of the spectrum because what you typically see over time is in the six months before, during and after a bear market or correction growth typically leads," said Bell.

During the last correction from May 2015 to February 2016, the S&P 500 declined by 14 percent. Over the next six months, the IVW growth ETF rallied 19 percent.

DisclaimerSaturday, March 16, 2019

Why Snap Stock Jumped Today

Shares of Snap (NYSE:SNAP) have jumped today, up by 11% as of 11:30 a.m. EDT, after the company received an upgrade from BTIG Research. Analyst Rich Greenfield has been a vocal skeptic of the Snapchat parent's turnaround prospects but is now changing his tune.

So whatBTIG had previously cut its rating on Snap to sell back in September, and then moved to the sidelines with a neutral rating in December. Greenfield is now boosting his rating to a buy with a $15 price target, despite noting that "virtually everything that could go wrong for Snapchat over the past couple years since going public has gone wrong." However, the analyst is encouraged that there has been a noticeable uptick in spending in North America by advertisers based in emerging markets, potentially taking advantage of low ad prices.

Image source: Snap.

There has also been a noticeable improvement in the quality of ads in Snapchat's Discover section, with a "meaningful reduction in clickbait/seedy influencer content and an increase in premium/publisher content," according to Greenfield. Snapchat remains incredibly popular with core users who use the platform for communications, and Snapchat still has potential to expand internationally. The company's progress in improving the app's performance on Android is also a welcome sign.

Now whatBTIG still has some reservations, most notably the investigations by the U.S. Department of Justice and the SEC over IPO disclosures. The outcome of those investigations could hurt Snap's cash position.

Greenfield has adjusted his estimates, and now expects negative free cash flow of just $510 million. He no longer believes that Snap will need to raise capital in 2020. The analyst is now modeling for 2019 revenue of $1.65 billion, up from a prior estimate of $1.4 billion. Looking farther out, Greenfield expects 2022 revenue to be $3.4 billion, up from a prior estimate of $2.1 billion.

Friday, March 15, 2019

Polar Capital LLP Has $67.97 Million Stake in Suncor Energy Inc. (SU)

![]() Polar Capital LLP lessened its stake in shares of Suncor Energy Inc. (NYSE:SU) (TSE:SU) by 21.3% in the fourth quarter, according to the company in its most recent Form 13F filing with the SEC. The firm owned 1,998,048 shares of the oil and gas producer’s stock after selling 541,874 shares during the quarter. Polar Capital LLP owned approximately 0.13% of Suncor Energy worth $67,965,000 at the end of the most recent quarter.

Polar Capital LLP lessened its stake in shares of Suncor Energy Inc. (NYSE:SU) (TSE:SU) by 21.3% in the fourth quarter, according to the company in its most recent Form 13F filing with the SEC. The firm owned 1,998,048 shares of the oil and gas producer’s stock after selling 541,874 shares during the quarter. Polar Capital LLP owned approximately 0.13% of Suncor Energy worth $67,965,000 at the end of the most recent quarter.

Several other large investors also recently added to or reduced their stakes in SU. First Manhattan Co. lifted its stake in Suncor Energy by 64.8% in the fourth quarter. First Manhattan Co. now owns 37,782 shares of the oil and gas producer’s stock worth $1,056,000 after acquiring an additional 14,856 shares during the period. Captrust Financial Advisors increased its holdings in shares of Suncor Energy by 184.4% during the third quarter. Captrust Financial Advisors now owns 17,626 shares of the oil and gas producer’s stock valued at $682,000 after acquiring an additional 11,429 shares in the last quarter. Marshall Wace LLP bought a new position in shares of Suncor Energy during the third quarter valued at $1,576,000. Morgan Stanley increased its holdings in shares of Suncor Energy by 23.1% during the third quarter. Morgan Stanley now owns 3,400,893 shares of the oil and gas producer’s stock valued at $131,579,000 after acquiring an additional 637,520 shares in the last quarter. Finally, Legacy Bridge LLC bought a new position in shares of Suncor Energy during the fourth quarter valued at $27,000. 66.63% of the stock is owned by hedge funds and other institutional investors.

Get Suncor Energy alerts:Several equities analysts have recently weighed in on SU shares. Zacks Investment Research restated a “hold” rating on shares of Suncor Energy in a report on Friday, November 16th. Canaccord Genuity set a $65.00 price target on Suncor Energy and gave the company a “buy” rating in a report on Tuesday, November 20th. Mizuho restated an “average” rating and set a $52.00 price target on shares of Suncor Energy in a report on Monday, December 3rd. Macquarie downgraded Suncor Energy from an “outperform” rating to a “neutral” rating and set a $46.00 price target for the company. in a report on Tuesday, December 4th. Finally, GMP Securities downgraded Suncor Energy from a “buy” rating to a “hold” rating in a report on Thursday, December 13th. One analyst has rated the stock with a sell rating, five have given a hold rating and eleven have assigned a buy rating to the stock. The stock currently has an average rating of “Buy” and a consensus target price of $49.12.

NYSE SU opened at $33.46 on Wednesday. Suncor Energy Inc. has a one year low of $25.81 and a one year high of $42.55. The stock has a market capitalization of $53.03 billion, a P/E ratio of 16.73, a price-to-earnings-growth ratio of 2.04 and a beta of 1.14. The company has a quick ratio of 0.54, a current ratio of 0.84 and a debt-to-equity ratio of 0.32.

Suncor Energy (NYSE:SU) (TSE:SU) last released its quarterly earnings data on Tuesday, February 5th. The oil and gas producer reported $0.27 EPS for the quarter, missing the consensus estimate of $0.38 by ($0.11). Suncor Energy had a return on equity of 9.50% and a net margin of 8.48%. The business had revenue of $6.77 billion during the quarter, compared to the consensus estimate of $8.13 billion. On average, sell-side analysts expect that Suncor Energy Inc. will post 1.83 EPS for the current year.

The firm also recently disclosed a quarterly dividend, which will be paid on Monday, March 25th. Investors of record on Monday, March 4th will be issued a $0.32 dividend. This represents a $1.28 annualized dividend and a yield of 3.83%. This is an increase from Suncor Energy’s previous quarterly dividend of $0.27. The ex-dividend date of this dividend is Friday, March 1st. Suncor Energy’s dividend payout ratio (DPR) is presently 54.00%.

TRADEMARK VIOLATION NOTICE: “Polar Capital LLP Has $67.97 Million Stake in Suncor Energy Inc. (SU)” was first reported by Ticker Report and is the sole property of of Ticker Report. If you are reading this report on another website, it was copied illegally and reposted in violation of US & international trademark & copyright laws. The correct version of this report can be read at https://www.tickerreport.com/banking-finance/4218874/polar-capital-llp-has-67-97-million-stake-in-suncor-energy-inc-su.html.

Suncor Energy Profile

Suncor Energy Inc operates as an integrated energy company. The company primarily focuses on developing petroleum resource basins in Canada's Athabasca oil sands; explores, acquires, develops, produces, and markets crude oil and natural gas in Canada and internationally; transports and refines crude oil; markets petroleum and petrochemical products primarily in Canada.

See Also: What are different types of coverage ratios?

Want to see what other hedge funds are holding SU? Visit HoldingsChannel.com to get the latest 13F filings and insider trades for Suncor Energy Inc. (NYSE:SU) (TSE:SU).

Thursday, March 14, 2019

BioSig Technologies Inc (BSGM) Given Average Recommendation of “Strong Buy” by Analysts

Shares of BioSig Technologies Inc (NASDAQ:BSGM) have earned an average broker rating score of 1.00 (Strong Buy) from the one brokers that provide coverage for the stock, Zacks Investment Research reports. One equities research analyst has rated the stock with a strong buy rating.

Shares of BioSig Technologies Inc (NASDAQ:BSGM) have earned an average broker rating score of 1.00 (Strong Buy) from the one brokers that provide coverage for the stock, Zacks Investment Research reports. One equities research analyst has rated the stock with a strong buy rating.

Analysts have set a 12 month consensus target price of $11.88 for the company, according to Zacks. Zacks has also assigned BioSig Technologies an industry rank of 70 out of 255 based on the ratings given to its competitors.

Get BioSig Technologies alerts:Several analysts have issued reports on BSGM shares. Laidlaw set a $11.00 price objective on shares of BioSig Technologies and gave the company a “buy” rating in a research report on Wednesday, February 20th. Roth Capital began coverage on shares of BioSig Technologies in a research report on Thursday, December 6th. They set a “buy” rating and a $14.00 price target for the company. Finally, Zacks Investment Research downgraded shares of BioSig Technologies from a “buy” rating to a “hold” rating in a research report on Monday, November 19th.

NASDAQ:BSGM traded up $0.04 during trading hours on Tuesday, hitting $5.55. The stock had a trading volume of 15,928 shares, compared to its average volume of 52,062. BioSig Technologies has a 1-year low of $3.38 and a 1-year high of $7.88.

In related news, CEO Kenneth L. Londoner bought 8,500 shares of the business’s stock in a transaction on Thursday, January 10th. The shares were bought at an average cost of $4.38 per share, for a total transaction of $37,230.00. The transaction was disclosed in a document filed with the Securities & Exchange Commission, which is accessible through this hyperlink. Also, CEO Kenneth L. Londoner bought 18,700 shares of the business’s stock in a transaction on Tuesday, January 22nd. The stock was bought at an average price of $4.35 per share, for a total transaction of $81,345.00. The disclosure for this purchase can be found here. 26.70% of the stock is currently owned by company insiders.

A hedge fund recently bought a new stake in BioSig Technologies stock. Millennium Management LLC bought a new position in shares of BioSig Technologies Inc (NASDAQ:BSGM) during the fourth quarter, according to its most recent disclosure with the Securities and Exchange Commission (SEC). The fund bought 156,822 shares of the company’s stock, valued at approximately $670,000. Millennium Management LLC owned 0.94% of BioSig Technologies as of its most recent SEC filing. 2.15% of the stock is owned by institutional investors.

About BioSig Technologies

BioSig Technologies, Inc, a development stage medical device company, engages in developing a proprietary biomedical signal processing technology platform to extract information from physiologic signals. Its product is PURE (Precise Uninterrupted Real-time evaluation of Electrograms) EP System, a surface electrocardiogram and intracardiac multichannel recording and analysis system that acquires, processes, and displays electrocardiogram and electrograms required during electrophysiology studies and catheter ablation procedures.

Read More: How Important is Technical Analysis of Stocks

Get a free copy of the Zacks research report on BioSig Technologies (BSGM)

For more information about research offerings from Zacks Investment Research, visit Zacks.com

Tuesday, March 12, 2019

BlackRock Inc. Acquires 21,077 Shares of Korn Ferry (KFY)

![]() BlackRock Inc. grew its holdings in shares of Korn Ferry (NYSE:KFY) by 0.2% during the fourth quarter, according to its most recent filing with the Securities and Exchange Commission. The institutional investor owned 8,602,101 shares of the business services provider’s stock after purchasing an additional 21,077 shares during the quarter. BlackRock Inc. owned about 0.15% of Korn Ferry worth $340,126,000 as of its most recent filing with the Securities and Exchange Commission.

BlackRock Inc. grew its holdings in shares of Korn Ferry (NYSE:KFY) by 0.2% during the fourth quarter, according to its most recent filing with the Securities and Exchange Commission. The institutional investor owned 8,602,101 shares of the business services provider’s stock after purchasing an additional 21,077 shares during the quarter. BlackRock Inc. owned about 0.15% of Korn Ferry worth $340,126,000 as of its most recent filing with the Securities and Exchange Commission.

Several other institutional investors have also added to or reduced their stakes in the company. California Public Employees Retirement System grew its position in Korn Ferry by 34.1% in the 4th quarter. California Public Employees Retirement System now owns 146,810 shares of the business services provider’s stock worth $5,805,000 after purchasing an additional 37,325 shares during the last quarter. Seizert Capital Partners LLC boosted its position in shares of Korn Ferry by 43.7% during the 4th quarter. Seizert Capital Partners LLC now owns 44,578 shares of the business services provider’s stock valued at $1,763,000 after acquiring an additional 13,565 shares in the last quarter. 361 Capital LLC boosted its position in shares of Korn Ferry by 70.7% during the 4th quarter. 361 Capital LLC now owns 49,212 shares of the business services provider’s stock valued at $1,946,000 after acquiring an additional 20,380 shares in the last quarter. Beacon Investment Advisory Services Inc. acquired a new stake in shares of Korn Ferry during the 4th quarter valued at about $206,000. Finally, PNC Financial Services Group Inc. boosted its position in shares of Korn Ferry by 22.5% during the 4th quarter. PNC Financial Services Group Inc. now owns 6,066 shares of the business services provider’s stock valued at $240,000 after acquiring an additional 1,113 shares in the last quarter. Institutional investors and hedge funds own 92.15% of the company’s stock.

Get Korn Ferry alerts:Several brokerages have recently weighed in on KFY. ValuEngine upgraded shares of Korn Ferry from a “sell” rating to a “hold” rating in a research report on Wednesday, January 2nd. Zacks Investment Research upgraded shares of Korn Ferry from a “hold” rating to a “buy” rating and set a $50.00 target price on the stock in a research report on Saturday, December 8th. Credit Suisse Group decreased their target price on shares of Korn Ferry from $44.00 to $40.00 and set an “underperform” rating on the stock in a research report on Friday, December 7th. SunTrust Banks decreased their target price on shares of Korn Ferry to $63.00 and set a “buy” rating on the stock in a research report on Friday, December 7th. Finally, TheStreet upgraded shares of Korn Ferry from a “c” rating to a “b” rating in a research report on Friday, December 7th. One equities research analyst has rated the stock with a sell rating, two have given a hold rating and three have assigned a buy rating to the company. Korn Ferry has a consensus rating of “Hold” and an average target price of $58.25.

Shares of KFY stock opened at $46.45 on Tuesday. Korn Ferry has a 12-month low of $37.38 and a 12-month high of $68.98. The stock has a market cap of $2.53 billion, a P/E ratio of 17.08 and a beta of 1.31. The company has a quick ratio of 2.00, a current ratio of 2.00 and a debt-to-equity ratio of 0.17.

Korn Ferry (NYSE:KFY) last announced its quarterly earnings results on Thursday, March 7th. The business services provider reported $0.81 earnings per share (EPS) for the quarter, meeting the consensus estimate of $0.81. Korn Ferry had a net margin of 3.92% and a return on equity of 15.01%. The firm had revenue of $474.50 million during the quarter, compared to the consensus estimate of $481.98 million. During the same period last year, the firm posted $0.70 EPS. On average, equities research analysts expect that Korn Ferry will post 3.36 EPS for the current fiscal year.

The company also recently declared a quarterly dividend, which will be paid on Monday, April 15th. Investors of record on Tuesday, March 26th will be issued a dividend of $0.10 per share. This represents a $0.40 annualized dividend and a yield of 0.86%. The ex-dividend date of this dividend is Monday, March 25th. Korn Ferry’s dividend payout ratio is currently 14.71%.

TRADEMARK VIOLATION WARNING: This report was first posted by Ticker Report and is the property of of Ticker Report. If you are reading this report on another publication, it was stolen and reposted in violation of United States and international trademark and copyright law. The original version of this report can be viewed at https://www.tickerreport.com/banking-finance/4215057/blackrock-inc-acquires-21077-shares-of-korn-ferry-kfy.html.

Korn Ferry Company Profile

Korn/Ferry International engages in the provision of global organizational consulting firm. It operates through the following segments: Executive Search, Hay Group, Futurestep, and Corporate. The Executive Search segment helps clients attract and hire leaders who fit in with their organization, and make it stand out.

Read More: Stop Order Uses For Individual Investors

Want to see what other hedge funds are holding KFY? Visit HoldingsChannel.com to get the latest 13F filings and insider trades for Korn Ferry (NYSE:KFY).

A Foolish Take: The Bull Market Turns 10

Over the weekend, investors celebrated the 10th anniversary of the stock market's lowest point during the bear market of 2008-2009. The S&P 500 (SNPINDEX:^GSPC) and the Dow Jones Industrial Average (DJINDICES:^DJI) hit their lowest points on March 9, 2009, before mounting a decade-long bull market that sent shares to unprecedented levels.

The financial crisis that brought about the stock market's plunge stemmed from the end of the housing boom in the U.S. during the mid-2000s. With many banks having extended credit on dubious terms to mortgage borrowers, the big drop in housing prices in many key markets across the nation created problems for lenders. Even the largest financial institutions proved undercapitalized to withstand the pressures that the housing bust created, sending shock waves throughout the global financial system, and it took massive government bailouts to ensure that big banks would be able to make it through the toughest part of the crisis.

Since then, the stock market has seen strong returns, but they haven't been equally strong everywhere. As you can see below, various market measures have given investors very different returns.

Data source: YCharts. Note: Returns shown are total returns for exchange-traded funds tracking the markets indicated. EAFE = Europe, Australasia, and Far East. EM = emerging markets.

A few points are worth noting. First, international markets have dramatically underperformed U.S. stocks over the past decade, as many foreign economies have gone through their own regional crises of confidence. That's been evident both in developed markets in areas like Western Europe and in emerging markets across China, India, Brazil, and Russia.

Second, in the U.S., the Nasdaq has been the big winner, with gains far outpacing those of other benchmarks. That's due in large part to the surge in technology stocks, which have done better than the broader market and produced some of the biggest winners of the past decade.

Finally, it's interesting to see that the Dow's and S&P's returns are almost identical. There's been plenty of discussion over the years about how the Dow's old-fashioned price-weighted calculation makes it a misleading indicator of stock performance, but over the long haul, it's tracked market-cap-weighted measures like the S&P quite closely.

In the decade to come, it's unlikely that investors will see stock market returns that come close to matching the track record of past 10 years. But over the long run, the rise and fall of the stock market has produced returns that have helped millions reach their financial goals.

Monday, March 11, 2019

Why Estee Lauder Stock Jumped 15% Last Month

Shares of Estee Lauder (NYSE:EL) were rising last month after the cosmetics giant turned in a strong second-quarter earnings report. Like other beauty companies, Estee Lauder appears to be benefiting from surging sales in the prestige-beauty segment. According to data from S&P Global Market Intelligence, the stock finished February up 15%.

As the chart below shows, the bulk of the stock's gains in the month came at the beginning of February after the company reported earnings.

EL data by YCharts.

So whatEstee Lauder's stock rose 12% on Feb. 5 as the company announced second-quarter results, beating estimates on the top and bottom lines. A strong performance in China buoyed overall growth as constant-currency sales rose 20% in the Asia/Pacific region, and prestige beauty accelerated in China as the company gained share in that valuable market.

Image source: Getty Images.

Total revenue rose 7%, or 11% after adjusting for currency exchange and the new revenue recognition standard, to $4 billion, ahead of estimates of $3.92 billion. The company noted the strong growth of brands like Estee Lauder, La Mer, and MAC, and reported sales in the skin care category was up 18%.

With the help of a lower tax rate, adjusted earnings per share rose from $1.52 to $1.86, easily beating expectations of $1.54. CEO Fabrizio Freda said: "We delivered an excellent performance in our fiscal second quarter. Importantly, this was our eighth consecutive quarter of impressive net sales growth that met or exceeded our long-term goal, all while navigating many global macro issues."

Now whatEstee Lauder also lifted its full-year guidance for the year, calling for sales to increase 5% to 6%, up from a prior forecast of 4% to 5%. Excluding currency exchange and the new revenue recognition standard, the company sees revenue rising 8% to 9% for the year.

On the bottom line, it now expects adjusted earnings per share of between $4.92 and $5, up from a previous range of $4.73 to $4.82 and higher than the $4.51 it reported last year. With tailwinds in China, skin care, and overall prestige beauty, Estee Lauder looks poised to deliver more solid growth.

Saturday, March 9, 2019

Insider Selling: Paycom Software Inc (PAYC) CFO Sells 12,000 Shares of Stock

![]() Paycom Software Inc (NYSE:PAYC) CFO Craig E. Boelte sold 12,000 shares of the firm’s stock in a transaction dated Wednesday, March 6th. The stock was sold at an average price of $176.03, for a total value of $2,112,360.00. The transaction was disclosed in a legal filing with the Securities & Exchange Commission, which is accessible through the SEC website.

Paycom Software Inc (NYSE:PAYC) CFO Craig E. Boelte sold 12,000 shares of the firm’s stock in a transaction dated Wednesday, March 6th. The stock was sold at an average price of $176.03, for a total value of $2,112,360.00. The transaction was disclosed in a legal filing with the Securities & Exchange Commission, which is accessible through the SEC website.

Craig E. Boelte also recently made the following trade(s):

Get Paycom Software alerts: On Wednesday, January 9th, Craig E. Boelte sold 12,000 shares of Paycom Software stock. The stock was sold at an average price of $128.78, for a total value of $1,545,360.00.Shares of NYSE:PAYC traded up $1.85 during mid-day trading on Friday, hitting $178.08. 481,080 shares of the company traded hands, compared to its average volume of 658,054. The company has a market cap of $10.33 billion, a P/E ratio of 81.69, a PEG ratio of 2.81 and a beta of 1.78. The company has a debt-to-equity ratio of 0.10, a quick ratio of 1.03 and a current ratio of 1.03. Paycom Software Inc has a 52-week low of $96.44 and a 52-week high of $186.00.

Paycom Software (NYSE:PAYC) last announced its earnings results on Tuesday, February 5th. The software maker reported $0.61 EPS for the quarter, beating the consensus estimate of $0.48 by $0.13. The business had revenue of $150.33 million for the quarter, compared to the consensus estimate of $144.10 million. Paycom Software had a return on equity of 38.83% and a net margin of 24.20%. The company’s revenue was up 31.8% on a year-over-year basis. During the same period last year, the business posted $0.90 EPS. Analysts predict that Paycom Software Inc will post 2.62 earnings per share for the current year.

Several large investors have recently made changes to their positions in PAYC. Vanguard Group Inc. grew its stake in Paycom Software by 2.2% during the 3rd quarter. Vanguard Group Inc. now owns 4,348,359 shares of the software maker’s stock valued at $675,778,000 after purchasing an additional 93,152 shares in the last quarter. Vanguard Group Inc grew its stake in Paycom Software by 2.2% during the 3rd quarter. Vanguard Group Inc now owns 4,348,359 shares of the software maker’s stock valued at $675,778,000 after purchasing an additional 93,152 shares in the last quarter. Capital International Investors acquired a new stake in Paycom Software during the 3rd quarter valued at approximately $488,601,000. BlackRock Inc. grew its stake in Paycom Software by 1.1% during the 4th quarter. BlackRock Inc. now owns 2,212,593 shares of the software maker’s stock valued at $270,933,000 after purchasing an additional 23,876 shares in the last quarter. Finally, Kayne Anderson Rudnick Investment Management LLC grew its stake in Paycom Software by 72.6% during the 4th quarter. Kayne Anderson Rudnick Investment Management LLC now owns 1,964,610 shares of the software maker’s stock valued at $240,566,000 after purchasing an additional 826,529 shares in the last quarter. Institutional investors and hedge funds own 79.35% of the company’s stock.

A number of equities analysts have recently commented on PAYC shares. Zacks Investment Research downgraded Paycom Software from a “buy” rating to a “hold” rating in a report on Wednesday, January 2nd. KeyCorp raised their price objective on Paycom Software from $133.00 to $182.00 and gave the stock an “overweight” rating in a report on Wednesday, February 6th. Royal Bank of Canada raised their price objective on Paycom Software to $139.00 and gave the stock a “market perform” rating in a report on Monday, February 4th. They noted that the move was a valuation call. Jefferies Financial Group raised their price objective on Paycom Software to $180.00 and gave the stock a “buy” rating in a report on Wednesday, February 6th. Finally, Canaccord Genuity raised their price objective on Paycom Software from $140.00 to $160.00 and gave the stock a “hold” rating in a report on Wednesday, February 6th. They noted that the move was a valuation call. Nine equities research analysts have rated the stock with a hold rating and seven have issued a buy rating to the stock. The company presently has a consensus rating of “Hold” and a consensus target price of $150.87.

WARNING: This piece of content was reported by Ticker Report and is the property of of Ticker Report. If you are accessing this piece of content on another domain, it was copied illegally and reposted in violation of US and international copyright and trademark legislation. The original version of this piece of content can be viewed at https://www.tickerreport.com/banking-finance/4207449/insider-selling-paycom-software-inc-payc-cfo-sells-12000-shares-of-stock.html.

Paycom Software Company Profile

Paycom Software, Inc provides cloud-based human capital management (HCM) software service for small to mid-sized companies in the United States. It provides functionality and data analytics that businesses need to manage the employment life cycle from recruitment to retirement. The company's HCM solution offers a suite of applications in the areas of talent acquisition, including applicant tracking, candidate tracker, background checks, on-boarding, e-verify, and tax credit services; and time and labor management, such as time and attendance, scheduling/schedule exchange, time-off requests, labor allocation, labor management reports/push reporting, and geofencing/geotracking.

Recommended Story: Trading Ex-Dividend Strategy

Catalyst Biosciences Inc (CBIO) Files 10-K for the Fiscal Year Ended on December 31, 2018

Catalyst Biosciences Inc (NASDAQ:CBIO) files its latest 10-K with SEC for the fiscal year ended on December 31, 2018. Catalyst Biosciences Inc is a clinical-stage biopharmaceutical company. The Company is engaged in creating and developing novel medicines to address serious medical conditions. Catalyst Biosciences Inc has a market cap of $93.880 million; its shares were traded at around $7.86 with and P/S ratio of 110.75. Catalyst Biosciences Inc had annual average EBITDA growth of 33.50% over the past five years.

For the latest fiscal year the company reported a revenue of $0.01 million, a decrease of 99.4% from the previous year. For the last five years Catalyst Biosciences Inc had an average revenue decline of 51.8% a year.The reported loss per diluted share was $2.68 for the year, compared with the loss per share of $269.849 in the previous year. The Catalyst Biosciences Inc had an operating margin of -563700%, compared with the operating margin of -2143.61% a year before. The 10-year historical median operating margin of Catalyst Biosciences Inc is -287.54%. The profitability rank of the company is 1 (out of 10).

At the end of the fiscal year, Catalyst Biosciences Inc has the cash and cash equivalents of $31.2 million, compared with $14.5 million in the previous year. The company had no long term debt. Catalyst Biosciences Inc has a financial strength rank of 8 (out of 10).

At the current stock price of $7.86, Catalyst Biosciences Inc is traded at 976.7% premium to its historical median P/S valuation band of $0.73. The P/S ratio of the stock is 110.75, while the historical median P/S ratio is 10.28. The stock lost 72.25% during the past 12 months.

For the complete 20-year historical financial data of CBIO, click here.

Friday, March 8, 2019

Buy AMC Shares If The Stock Dips

The last time I wrote about AMC Entertainment (AMC), I asked if the stock was a knife worth catching. Since then, the stock fell from $14.16 to as low as $11.66. But after the fourth quarter report, investors piled onto the stock. The company deserves the bullish buying thanks to stronger sequential results, but questions remain. Should the company pay a generous dividend when its balance sheet is burdened by debt? Will 2019 movie attendance add to revenue growth?

AMC benefited from strong movie title releases in 2018. Venom, Incredibles 2, Avengers: Infinity War and Black Panther led to strong movie attendance in the period. That the domestic entry box office reached a new all-time record of ~$12 billion will make this year's comparable results harder to match. Still, AMC's 6.1% attendance increase last year drove revenues to a record $5.5 billion. AMC's food and beverage revenue growth of 8% is a notable achievement because it lifted EBITDA by 13% Y/Y to $929.2 million last year.

Growth Drivers in 2019Theatre renovations will continue to drive revenue this year. In 2018, AMC enjoyed a return of above 25% with its recliner renovations. The response in Europe was even better, with returns of more than 50%.

AMC's mobile app and website benefited from higher online engagement. With online sales accounting for 45%, the company has room to derive even more sales from this channel. The operating cost model for online is likely better than offline and will add positively to 2019 EBITDA.

The AMC Stub A-List program continues to be of strategic importance, especially when Helios' (OTC:HMNY) MoviePass is not going away. The subscription helped AMC outpace sales in the industry domestically. The monthly prepaid subscription offering is incredibly successful because it launched just eight months ago. Stubs has 18.6 million member households. 45% of that clientele is using Stubs to track purchases at AMC and collecting the all-important loyalty points. AMC forecasts that it will send 1.5 billion e-mails and texts to Stub members.

AMC ended Q4 with 704,560 members on the A-List. Expect these members to add to AMC's profitability as moviegoers bring friends and family who pay full price, along with buying food and beverage at the theatres.

Strong Pricing PowerThanks to the demand inelasticity of the subscription, AMC raised membership prices by 13%. Investors may expect membership continuing to grow despite the price increase. Once again, because subscription moviegoers visit the theatre more often than non-members, AMC has the opportunity to grow overall attendance and make more profits from concession sales. A-List members spend around 2.5 times more on food and beverage compared to before signing up.

When AMC stock rallied to more than $16 following its fourth quarter report, investors may have become overly excited. Stubs A-List was EBITDA neutral to slightly positive in January and February. For every 1 million subscribers, AMC gets between $15 - $25 million in incremental adjusted EBITDA (annualized). The $11.6 million adjusted EBITDA in the second half of 2018 also is at the lower end of management's $10 - $15 million target. Despite subscription growth exceeding expectations but adding less than thought in 2018, AMC now forecasts A-List will add to EBITDA this year, one year ahead of schedule.

Subscription Model Key to Buying AMC StockInvestors who held Adobe Systems (ADBE) or Microsoft (MSFT) will recognize the contribution to profit growth when a company shifts from charging per unit to administering a subscription fee instead. Adobe's Acrobat subscription and Document Cloud, for example, added $800 million in revenue. Microsoft leveraged giving away Windows 10 by selling Office 365 subscriptions. Even though AMC will not enjoy the same profit margins as a software company, AMC would lead in this new model for the movie industry.

RisksAMC's 4.3 times debt/equity might trouble investors, especially when the stock's dividend yields 5.1%. If movie attendance falls due to poor movie title releases in 2019 or if the economy weakens, AMC's cash flow will fall. That would renew investor worries over the company's debt. At a time when the Fed has a bias to raise rates, holding high levels of debt would ultimately hurt AMC stockholders.

Valuation and Your TakeawaySix analysts cover AMC stock and have, on average, a $19.50 price target.

Source: Tipranks

After AMC's strong rally to above $16, near-term profit-taking pressure suggests investors may wait for a better entry point. If shares fall below $14, investors who missed last week's rally may start a position and wait for the next quarter's report.

Please [+]Follow me for coverage on deeply-discounted technology, under-covered stocks. Click on the "follow" button beside my avatar.

For a limited time, I am inviting readers to sign up for a risk-free, trial subscription to DIY (do-it-yourself) investing. This invitation will close after reaching capacity.

Disclosure: I/we have no positions in any stocks mentioned, but may initiate a long position in AMC over the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Thursday, March 7, 2019

Best Small Cap Stocks To Invest In 2019

Last week, small cap security stock Patriot One Technologies (OTCQB: PTOTF; TSE: PAT.V) announced that its bought deal financing, which increased in size to close to $11.5M in gross proceeds to the Company, with the financing deal set to become a big aid in business development. This includes helping to fund:

North American and UK development centers Product showrooms Security forum sponsorships Addition of leading experts to the teamPatriot One Technologies' award-winning PATSCAN CMR concealed weapons detection system is a first-of-its-kind Cognitive Microwave Radar concealed weapons detection system that is an effective tool to combat active shooter threats before they occur as its designed for cost-effective deployment in weapon-restricted buildings and facilities. The solution and related hardware can be installed in hallways and doorways to covertly identify weapons and to alert security of an active threat entering the premises. The owners/operators of private and certain public facilities can then prominently post anti-weapons policies with compliance being assured.

concealed weapons detection system is a first-of-its-kind Cognitive Microwave Radar concealed weapons detection system that is an effective tool to combat active shooter threats before they occur as its designed for cost-effective deployment in weapon-restricted buildings and facilities. The solution and related hardware can be installed in hallways and doorways to covertly identify weapons and to alert security of an active threat entering the premises. The owners/operators of private and certain public facilities can then prominently post anti-weapons policies with compliance being assured.

Best Small Cap Stocks To Invest In 2019: CoreSite Realty Corporation(COR)

Advisors' Opinion:- [By Shane Hupp]

CORION (CURRENCY:COR) traded 0.1% higher against the dollar during the 24 hour period ending at 11:00 AM Eastern on June 12th. One CORION token can currently be purchased for about $0.0711 or 0.00001050 BTC on exchanges. Over the last week, CORION has traded down 38.7% against the dollar. CORION has a total market capitalization of $0.00 and $1,404.00 worth of CORION was traded on exchanges in the last day.

- [By Jack Delaney]

Take CoreSite Realty Corp. (NYSE: COR), for example. The stock price not only climbed 43.66% from 2017 to 2018, but it also pays its shareholders a dividend of $3.92 per share.

- [By Logan Wallace]

CoreSite Realty Corp (NYSE:COR) – Research analysts at Jefferies Financial Group cut their Q3 2018 earnings estimates for shares of CoreSite Realty in a note issued to investors on Thursday, October 4th. Jefferies Financial Group analyst J. Petersen now anticipates that the real estate investment trust will earn $1.22 per share for the quarter, down from their prior estimate of $1.23. Jefferies Financial Group also issued estimates for CoreSite Realty’s FY2018 earnings at $5.04 EPS, FY2019 earnings at $5.44 EPS and FY2020 earnings at $5.94 EPS.

- [By Motley Fool Transcribers]

CoreSite Realty Corp (NYSE:COR)Q4 2018 Earnings Conference CallFeb. 07, 2019, 12:00 p.m. ET

Contents: Prepared Remarks Questions and Answers Call Participants Prepared Remarks:Operator

- [By Joseph Griffin]

CORION (CURRENCY:COR) traded down 7% against the US dollar during the one day period ending at 14:00 PM Eastern on July 1st. Over the last week, CORION has traded 6.7% lower against the US dollar. One CORION token can currently be bought for approximately $0.0601 or 0.00000950 BTC on exchanges. CORION has a total market capitalization of $0.00 and $960.00 worth of CORION was traded on exchanges in the last day.

Best Small Cap Stocks To Invest In 2019: Euro Tech Holdings Company Limited(CLWT)

Advisors' Opinion:- [By Lisa Levin] Gainers Euro Tech Holdings Company Limited (NASDAQ: CLWT) surged 73.3 percent to $3.90. Integrated Media Technology Limited (NASDAQ: IMTE) shares gained 51 percent to $33.1365. The nano-cap low-float stock skyrocketed over 1,300 percent on Wednesday on no company specific news which would support the surge. The move higher is consistent with what was seen in other low-float stocks over the past few months. Monaker Group, Inc. (NASDAQ: MKGI) shares jumped 34 percent to $3.00. Sharing Economy International Inc. (NASDAQ: SEII) shares rose 28.2 percent to $4.51 after gaining 9.32 percent on Wednesday. STAAR Surgical Company (NASDAQ: STAA) shares jumped 27.8 percent to $21.40 after reporting upbeat Q1 results. Boxlight Corporation (NASDAQ: BOXL) rose 20.5 percent to $8.920 after climbing 107.87 percent on Wednesday. Xspand Products Lab Inc (NASDAQ: XSPL) gained 19.5 percent to $ 5.97. Xspand Products priced its IPO at $5 per share. YRC Worldwide Inc. (NASDAQ: YRCW) rose 18.9 percent to $10.035 following upbeat quarterly earnings. ENDRA Life Sciences Inc. (NASDAQ: NDRA) gained 18.3 percent to $3.0177. ENDRA Life Sciences is expected to report Q1 results on May 15. MYR Group Inc. (NASDAQ: MYRG) rose 18.1 percent to $35.85 after the company posted strong Q1 earnings. Rudolph Technologies, Inc. (NASDAQ: RTEC) shares jumped 16 percent to $30.75 following upbeat quarterly earnings. TTM Technologies, Inc. (NASDAQ: TTMI) gained 13.7 percent to $16.53 after reporting Q1 results. Insight Enterprises, Inc. (NASDAQ: NSIT) shares surged 12 percent to $40.06 following better-than-expected Q1 earnings. TreeHouse Foods, Inc. (NYSE: THS) rose 11.8 percent to $40.93 following Q1 results. Engility Holdings, Inc. (NYSE: EGL) surged 11.2 percent to $27.36. Engility reported upbeat quarterly earnings. Synalloy Corporation (NASDAQ: SYNL) rose 10.7 percent to $19.10 following Q1 results. Logitech International S.A. (NASDAQ: LOGI)

- [By Lisa Levin]

Euro Tech Holdings Company Limited (NASDAQ: CLWT) shares shot up 49 percent to $4.775 after reporting 2017 year-end results.

Shares of Medigus Ltd. (NASDAQ: MDGS) got a boost, shooting up 34 percent to $1.5092 in reaction to its Monday announcement of a distribution agreement. The medical device company said it reached an agreement to distribute its minimally invasive medical devices in Turkey, Azerbaijan and Georgia.

- [By Lisa Levin] Gainers Euro Tech Holdings Company Limited (NASDAQ: CLWT) shares rose 14.1 percent to $3.65 in the pre-market trading session after reporting 2017 year-end results. LightPath Technologies, Inc. (NASDAQ: LPTH) rose 13.3 percent to $2.43 in pre-market trading after reporting a third-quarter earnings beat. MYnd Analytics, Inc. (NASDAQ: MYND) rose 10.5 percent to $3.49 in pre-market trading. MYnd Analytics reported a Q2 net loss of $2.7 million on revenue of $459,900. SORL Auto Parts, Inc. (NASDAQ: SORL) shares rose 8.4 percent to $5.68 in pre-market trading after reporting upbeat Q1 results. Famous Dave's of America, Inc. (NASDAQ: DAVE) shares rose 7.7 percent to $8.40 in pre-market trading after the company reported upbeat earnings for its first quarter on Monday. Xenon Pharmaceuticals Inc. (NASDAQ: XENE) rose 7.5 percent to $6.45 in pre-market trading after the company presented XEN901 Phase 1 clinical update and XEN1101 TMS pharmacodynamic Phase 1 data. Mimecast Ltd (NASDAQ: MIME) rose 6.5 percent to $43.50 in pre-market trading following a first-quarter sales beat. Boxlight Corporation (NASDAQ: BOXL) rose 6 percent to $12.50 in pre-market trading after surging 77.44 percent on Monday. Intellia Therapeutics, Inc. (NASDAQ: NTLA) shares rose 6 percent to $26.05 in pre-market trading after climbing 3.58 percent on Monday. PPDAI Group Inc. (NASDAQ: PPDF) rose 4.7 percent to $7.20 in pre-market trading following Q1 results. Xunlei Limited (NASDAQ: XNET) rose 4.1 percent to $13.88 in pre-market trading after gaining 2.54 percent on Monday. Valeant Pharmaceuticals International, Inc. (NYSE: VRX) shares rose 4.5 percent to $21.73 in pre-market trading. Mizuho upgraded Valeant from Neutral to Buy. Bovie Medical Corporation (NYSE: BVX) rose 4.1 percent to $3.80 in pre-market trading after reporting a first-quarter sales beat. Myomo, Inc. (NYSE: MYO) rose 3.4 percent to $4.00 in pre-market trading after jumping 23.25 percent o

- [By Lisa Levin] Gainers Portola Pharmaceuticals, Inc. (NASDAQ: PTLA) rose 34.7 percent to $45.50 in pre-market trading following news that the FDA has approved Andexxa for the reversal of factor Xa inhibitors. Euro Tech Holdings Company Limited (NASDAQ: CLWT) rose 15.7 percent to $6.65 in pre-market trading after climbing 155.56 percent on Thursday. China Recycling Energy Corporation (NASDAQ: CREG) rose 14.7 percent to $2.75 in pre-market trading after climbing 57.89 percent on Thursday. Pandora Media, Inc. (NYSE: P) rose 11 percent to $6.40 in pre-market trading after reporting strong quarterly results. Fred's, Inc. (NASDAQ: FRED) rose 9.2 percent to $1.90 in pre-market trading following Q4 results. Shake Shack Inc (NYSE: SHAK) rose 9.1 percent to $51.70 in pre-market trading after the company reported upbeat results for its first quarter and raised its FY18 guidance. Allscripts Healthcare Solutions, Inc. (NASDAQ: MDRX) rose 9 percent to $12.55 in pre-market trading after the company posted Q1 results and agreed to acquire HealthGrid. Weight Watchers International, Inc. (NYSE: WTW) rose 7.6 percent to $75 in pre-market trading after the company reported stronger-than-expected results for its first quarter. The company also raised its FY18 earnings outlook from $2.40-$2.70 to $3-$3.20. Viavi Solutions Inc. (NASDAQ: VIAV) rose 7.5 percent to $10.15 in pre-market trading following Q3 results. Pearson plc (NYSE: PSO) rose 4.5 percent to $11.83 in pre-market trading after reporting strong quarterly earnings. Alibaba Group Holding Ltd (NYSE: BABA) shares rose 4.4 percent to $190.50 in the pre-market trading session as the company posted upbeat Q4 results. Aqua Metals, Inc. (NASDAQ: AQMS) shares rose 3.9 percent to $4.30 in pre-market trading after gaining 6.98 percent on Thursday. Newell Brands Inc (NYSE: NWL) shares rose 3.6 percent to $27.65 in pre-market trading after reporting upbeat quarterly earnings. HMS Holdings Corp (NASDAQ: H

- [By Lisa Levin]

Euro Tech Holdings Company Limited (NASDAQ: CLWT) was down, falling around 7 percent to $3.745 after dropping 30.26 percent on Friday.

Commodities

- [By Lisa Levin]

Euro Tech Holdings Company Limited (NASDAQ: CLWT) shares shot up 35 percent to $5.20 after the company declared a $0.70 per share special dividend.

Best Small Cap Stocks To Invest In 2019: SodaStream International Ltd.(SODA)

Advisors' Opinion:- [By Jeremy Bowman]

The SodaStream International (NASDAQ:SODA) stock story is coming to a close.

The Israeli maker of DIY sparkling-water machines has agreed to sell itself to PepsiCo (NASDAQ:PEP) for $144 a share or $3.2 billion, bringing to an end SodaStream's wild ride on the public markets.

- [By Rick Munarriz]

Sometimes it takes years for buyout chatter to finally materialize. PepsiCo (NASDAQ:PEP) is announcing that it will be acquiring SodaStream (NASDAQ:SODA) in an all-cash deal valued at $3.2 billion. Both boards have approved the transaction that will cash out SodaStream investors at $144 a share. The purchase is expected to close in January, as long as the majority of SodaStream shareholders vote in favor of the deal.

- [By Jeremy Bowman, Rich Smith, and John Bromels]

Buffett fans probably already have a sense of what kind of stocks the Oracle of Omaha like, but you may not have thought of these three. Keep reading to see why our contributors recommend ExxonMobil (NYSE:XOM), Comcast (NASDAQ:CMCSA), and SodaStream International (NASDAQ:SODA).

- [By Demitrios Kalogeropoulos]

SodaStream (NASDAQ:SODA) recently announced surprisingly strong first-quarter earnings as sales growth sped up to a 25% pace and profitability improved. The seller of at-home carbonated beverage machines is benefiting from a long-term trend of rising global demand for sparkling water.

- [By Jim Crumly]

As for individual stocks, PepsiCo (NASDAQ:PEP) announced plans to buy SodaStream International (NASDAQ:SODA), and The Estee Lauder Companies (NYSE:EL) reported better-than-expected sales and profit growth.

Wednesday, March 6, 2019

The Stories That We Tell

As a society, the stories that we tell, at a point in time, say a lot about who we are and what we believe. They create the zeitgeist&a;nbsp;that we look back on, and that in turn forms the age to come.

So in many ways, it is our responsibility to tell the stories that we wish to define us and our children. As we head towards &l;a href=&q;https://www.internationalwomensday.com/&q; target=&q;_blank&q;&g;International Women&s;s Day 2019&l;/a&g;,&a;nbsp;many of us are&a;nbsp;asking ourselves, are the stories we are telling those that we wish to be remembered for?

When it comes to female empowerment through business and entrepreneurship, I think the answer is a resounding no. If you look the 21st century way for stories - so if you Google - for the word Entrepreneur, you will not see female faces. Entrepreneurial stories are predominantly male, with a male-led narrative and a masculine protagonist.&a;nbsp;Female businesses are seen as fluffy, cupcake or caring businesses, with &l;a href=&q;https://www.british-business-bank.co.uk/uk-vc-female-founders-report/&q; target=&q;_blank&q;&g;little serious investment going into them&l;/a&g; and therefore not worthy of being part of the story.

This is what we need to change - and we can change. We can decide as a&a;nbsp;culture to tell different stories - and they are all out there waiting to be told. And in many cases, they are much more interesting, full of depth, overcoming adversity and with a heroine worth cheering for.

Ahead of International Women&s;s Day, we are starting to hear these stories more from many quarters, including &l;a href=&q;http://f-entrepreneur.com/fentrepreneur-top-100/&q; target=&q;_blank&q;&g;f:Entrepreneur&s;s 100 #ialso stories&l;/a&g; of female led businesses that are doing way more exciting and interesting things than &q;just&q; starting a business. We should not confine this to just a week in March. We should be telling these stories every day. This is what will inspire the next generation - of men and women.

&l;img class=&q;size-full wp-image-32&q; src=&q;http://blogs-images.forbes.com/michelleovens/files/2019/03/Grace-Anighoro.jpg?width=960&q; alt=&q;&q; data-height=&q;765&q; data-width=&q;765&q;&g; Grace Anighoro, Founder of Marvellous Mix Chin Chin

Take the story of Grace Anighoro. She has a fabulous business called &l;a href=&q;https://www.marvellousmix.co.uk/&q; target=&q;_blank&q;&g;Marvellous Mix Chin Chin&l;/a&g; making pastry snacks. It is a start up that began at home and now ships much further afield. She is also a mother - a mother of a child with Osteogenesis Imperfecta - Brittle Bone Disease. Not only does she manage this on a day to day basis, but she has taken that experience to tutor other parents of children with special needs with the Department of Public Health in Greenwich. Understanding the challenges many women go through, she then went onto start the Marvellous Girls Club Ltd. This is a club for young girls and teenagers and encourages them to grow up to be confident, pursue their dreams and reach their potential. This is a business with a story worth telling.

&l;img class=&q;size-large wp-image-33&q; src=&q;http://blogs-images.forbes.com/michelleovens/files/2019/03/Clare-Talbot-Jones--1200x1200.jpg?width=960&q; alt=&q;&q; data-height=&q;1200&q; data-width=&q;1200&q;&g; Clare Talbot-Jones, Talbot Jones Risk Solutions

It is not just about&a;nbsp;snacks and caring roles, as the story of Clare Talbot-Jones from Gateshead shows us too. Running a &l;a href=&q;https://talbotjones.co.uk/&q; target=&q;_blank&q;&g;commercial insurance broker&l;/a&g; focused on the third sector, Clare is a tech and financial services entrepreneur, but with a much richer story to tell. Recovering from serious illness, Clare came to her business with a drive to succeed and do something different. Clare is a mentor for the Millin Charity, an organisation that supports local women into self-employment. She works to remove the stigma of mental illness from the workplace and speaks at local events to promote her ethos. She has become disability confident, learnt sign language, and developed her own IP for a new piece of technology in her sector. Her story does not stop, as all the best stories do not. She continues to look for ways to benefit society and develop new business tools for herself and others.

When we look at who we are as a society,&a;nbsp;do these stories not tell us more about who we want to be? As women really come into an age where they can define their stories by their own rules, where diversity and equality means they can experience real freedom, we are seeing a wealth of phenomenal stories bubbling up from this previously un-tapped potential.

It is now our responsibility to tell more of these stories and to pass them on. This is how we ensure the businesses and generations of the future learn from and build on them. We want them to look back on this age with pride in what women have achieved and to see stories of female leadership held up equal to those of male achievement. This is equality.

These will be the stories that we will tell.&l;/p&g;

Monday, March 4, 2019

$23.08 Million in Sales Expected for AXT Inc (AXTI) This Quarter

![]() Wall Street analysts predict that AXT Inc (NASDAQ:AXTI) will report $23.08 million in sales for the current fiscal quarter, according to Zacks Investment Research. Three analysts have issued estimates for AXT’s earnings, with the highest sales estimate coming in at $24.22 million and the lowest estimate coming in at $22.03 million. AXT reported sales of $24.42 million in the same quarter last year, which indicates a negative year-over-year growth rate of 5.5%. The business is expected to report its next quarterly earnings report on Wednesday, April 24th.

Wall Street analysts predict that AXT Inc (NASDAQ:AXTI) will report $23.08 million in sales for the current fiscal quarter, according to Zacks Investment Research. Three analysts have issued estimates for AXT’s earnings, with the highest sales estimate coming in at $24.22 million and the lowest estimate coming in at $22.03 million. AXT reported sales of $24.42 million in the same quarter last year, which indicates a negative year-over-year growth rate of 5.5%. The business is expected to report its next quarterly earnings report on Wednesday, April 24th.

According to Zacks, analysts expect that AXT will report full-year sales of $102.46 million for the current fiscal year, with estimates ranging from $100.00 million to $107.37 million. For the next year, analysts forecast that the company will report sales of $114.50 million, with estimates ranging from $114.00 million to $115.00 million. Zacks’ sales averages are an average based on a survey of analysts that that provide coverage for AXT.

Get AXT alerts:AXT (NASDAQ:AXTI) last posted its earnings results on Wednesday, February 20th. The semiconductor company reported ($0.03) earnings per share for the quarter, missing the consensus estimate of $0.02 by ($0.05). The business had revenue of $22.20 million for the quarter, compared to analysts’ expectations of $22.21 million. AXT had a return on equity of 5.06% and a net margin of 9.43%. AXT’s revenue for the quarter was down 15.6% compared to the same quarter last year. During the same quarter in the previous year, the firm earned $0.08 EPS.

AXTI has been the topic of a number of recent research reports. Zacks Investment Research raised AXT from a “sell” rating to a “hold” rating in a report on Tuesday, December 18th. TheStreet lowered AXT from a “b-” rating to a “c+” rating in a report on Thursday, December 27th. Finally, ValuEngine upgraded shares of AXT from a “strong sell” rating to a “sell” rating in a research report on Wednesday, January 2nd. Three equities research analysts have rated the stock with a hold rating and three have given a buy rating to the company’s stock. The stock presently has a consensus rating of “Buy” and an average price target of $7.88.

Shares of NASDAQ:AXTI traded up $0.10 during trading on Wednesday, reaching $4.39. The company had a trading volume of 12,995 shares, compared to its average volume of 257,306. The firm has a market cap of $170.06 million, a P/E ratio of 18.29, a PEG ratio of 0.95 and a beta of 1.10. AXT has a fifty-two week low of $3.70 and a fifty-two week high of $9.38.